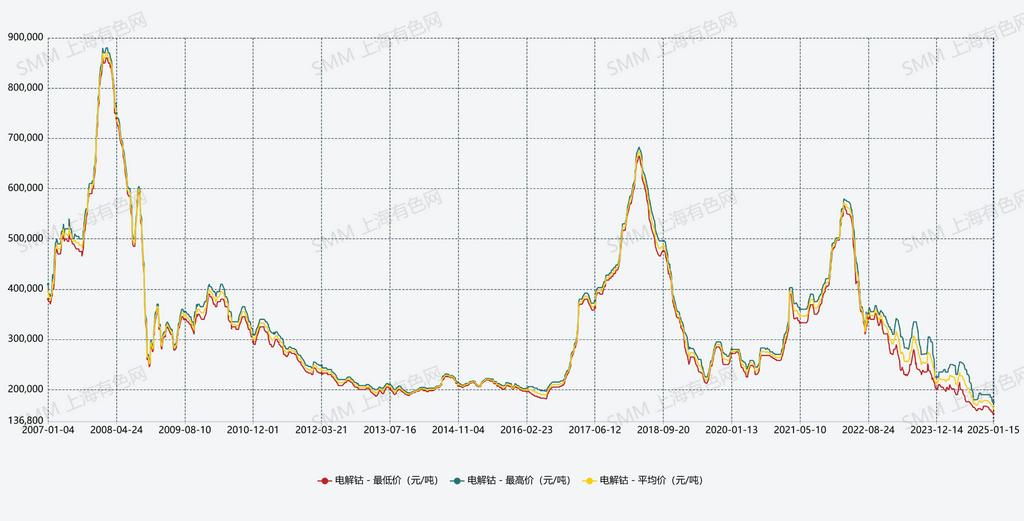

The annual average price of refined cobalt in China in 2024 was 201,700 yuan/mt, down 26% YoY compared to the same period in 2023. Breaking it down:

In Q1 2024, due to the impact of the Chinese New Year holiday, the market experienced weak supply and demand. On the supply side, as smelters' in-plant inventory of refined cobalt remained low, production maintained an upward trend. On the demand side, the market recovered slowly after the holiday, but demand fell short of expectations, and overall transactions were relatively sluggish.

In Q2 2024, the traditional "Golden March and Silver April" demand lagged, with only some traders engaging in buying the dip; actual end-use procurement was limited, while supply continued to increase, reversing the supply-demand balance for refined cobalt. Additionally, as the market held a bearish outlook on future raw material prices, the weakening cost support led to a decline in refined cobalt prices.

In Q3 2024, on the supply side, supported by fixed orders, smelters maintained high operating rates. On the demand side, the overseas summer break persisted, and domestic demand showed no improvement, with the overall market relying on long-term contract demand. Furthermore, as the prices of new brands were slightly lower than those of established enterprises, and end-use demand fell short of expectations, the oversupply situation intensified cut-throat competition in the industry, leading to a continued price decline.

In Q4 2024, due to the rapid release of capacity throughout the year, demand struggled to match the growth in supply, resulting in continuous inventory buildup. However, as smelters concentrated on deliveries at year-end, the availability of refined cobalt for circulation decreased, with a noticeable tendency to stand firm on quotes. Meanwhile, some just-in-time procurement from downstream end-use markets might further boost spot prices. Toward year-end, as the issue of overcapacity worsened, the oversupply situation caused spot prices to decline again.

On the supply side:

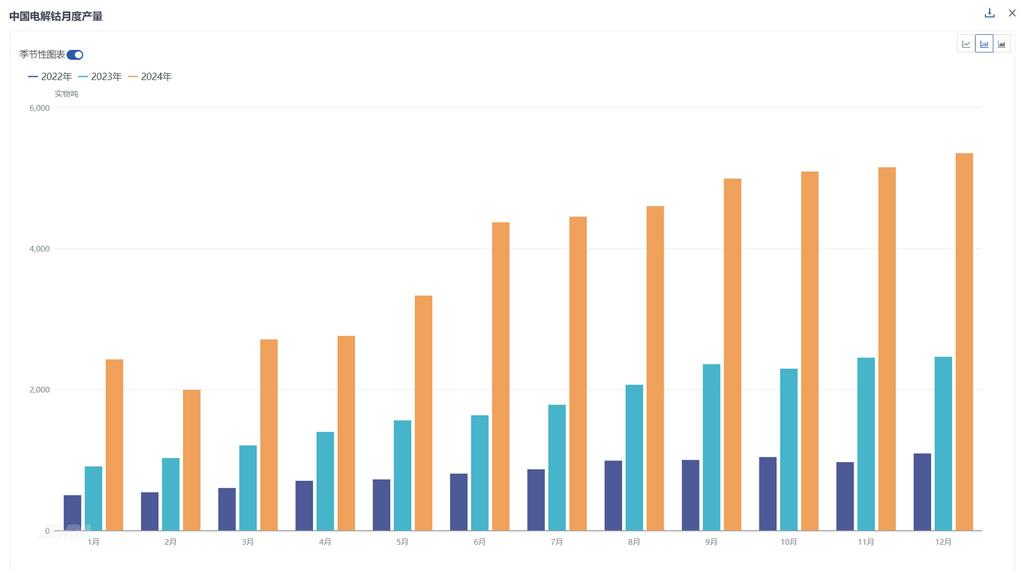

According to SMM data, China's refined cobalt production in 2024 was approximately 47,000 mt (metal content), up 123% YoY compared to the same period in 2023. In recent years, driven by the development of military and aerospace industries, China's refined cobalt capacity has gradually expanded. By the end of 2024, domestic refined cobalt capacity is expected to exceed 70,000 mt, representing a YoY increase of over 120% compared to 2023. Looking at the full year of 2024, due to the concentrated demand for cobalt salt in China and thin or near-loss margins, some cobalt salt enterprises were attracted to switch to refined cobalt production. Additionally, as refined cobalt remained relatively profitable among cobalt products, many new capacities entered the market, leading to a significant MoM increase in production in 2024.

On the demand side:

Refined cobalt is primarily used in high-temperature alloys, benefiting from the rapid development of China's aviation sector and the boost in demand from the military industry, which brought certain incremental demand to the cobalt-based high-temperature alloy market. The annual demand in 2024 is expected to increase significantly. Furthermore, refined cobalt is also used in the magnetic materials market, mainly driven by demand for samarium-cobalt magnets. In 2024, as samarium-cobalt permanent magnets are primarily applied in communication base stations, high-temperature motors, and other specialized motors, the market still holds certain growth potential.

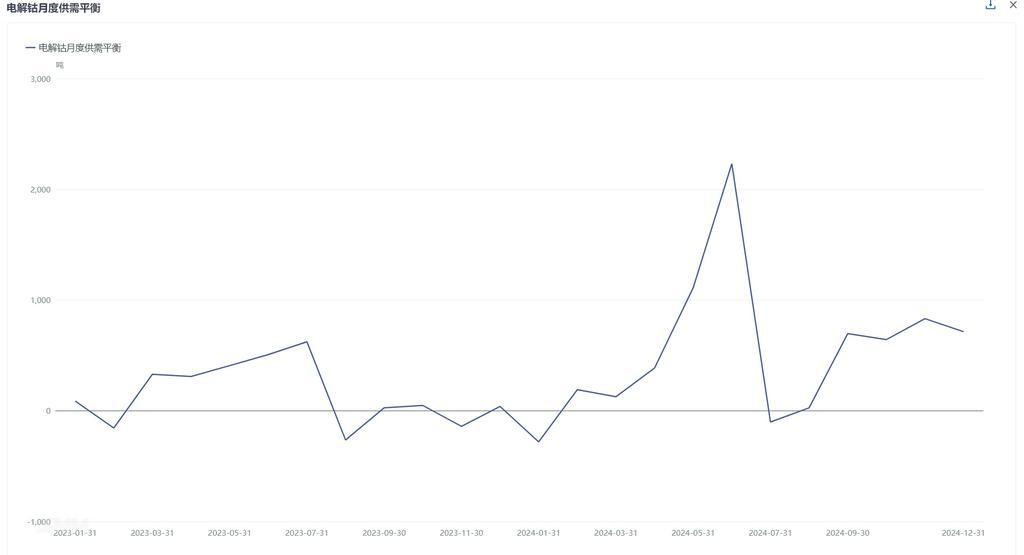

From a comprehensive supply and demand perspective:

In Q1 2024, on the supply side, affected by the Chinese New Year and the industry's off-season, refined cobalt production decreased significantly. On the demand side, the seasonal off-season might see some recovery starting in March. However, due to high social inventory levels, the price rebound was relatively small.

In Q2 2024, on the supply side, as refined cobalt remained profitable, the release of new capacity and ramp-up continued, maintaining an increase in production. On the demand side, demand for high-temperature alloys and magnetic materials recovered slower than expected, and the traditional "Golden March and Silver April" demand lagged. From a comprehensive supply and demand perspective, as the oversupply of refined cobalt widened, the price decline accelerated in Q2.

In Q3 2024, as traditional industry demand remained relatively fixed, the space for incremental demand was limited. However, due to the higher-than-expected fixed deliveries in H2, other incremental demand increased significantly, resulting in a notable increase in demand in Q3 and Q4 compared to Q1 and Q2. Meanwhile, as the market's capacity release outpaced demand growth, the oversupply situation caused spot prices to remain on a downward trend.

In Q4 2024, due to the rapid release of capacity throughout the year, demand struggled to match the growth in supply, resulting in continuous inventory buildup. However, as smelters concentrated on deliveries at year-end, the availability of refined cobalt for circulation decreased, with a noticeable tendency to stand firm on quotes. Meanwhile, some just-in-time procurement from downstream end-use markets might further boost spot prices. Toward year-end, as the issue of overcapacity worsened, the oversupply situation might cause spot prices to decline again.

Outlook for 2025:

After 2025, as the oversupply of refined cobalt persists, apart from a few mainstream brands planning to switch from cobalt salt production or add new capacity, other enterprises are unlikely to have additional plans. The long-term operating rate of the refined cobalt market is expected to decline, focusing on inventory digestion. Additionally, affected by the surplus of raw materials, refined cobalt production might remain at a high level. On the demand side, although downstream demand might see some growth, supply will far exceed demand, and the oversupply situation is expected to continue. Domestic spot prices and export prices of refined cobalt might experience varying degrees of decline.

SMM New Energy Research Team

Cong Wang 021-51666838

Rui Ma 021-51595780

Disheng Feng 021-51666714

Ying Xu 021-51666707

Yanlin Lü 021-20707875

Yujun Liu 021-20707895

Xiaodan Yu 021-20707870

Zhicheng Zhou 021-51666711